The UK construction and building materials sector is in the midst of a well-publicised supply chain crisis. It has been at the forefront of post-lockdown economic recovery, with its highest activity for many years. Soaring demand, coupled with supply-side production and distribution problems, has put a strain on availability of a number of core materials, with a consequential increase in price.

The situation has exposed the sector’s relative immaturity in concepts such as collaborative planning, forecasting and replenishment (CPFR), and vendor managed inventory (VMI). CPFR seeks a more cooperative and collaborative approach to managing inventory and replenishing products, but information must be co-ordinated through the supply chain and company sales and operational planning (S&OP) processes must be aligned. It offers significant potential benefits in efficiency and responsiveness of the entire end-to-end supply chain. Similarly, with VMI, where a partner company takes responsibility for supplying the necessary components and materials directly to the point of use, this realignment of responsibilities can ensure a more reliable and consistent supply of critical items.

Like VMI, modern methods of construction (MMC) aim to bring production line efficiency to the construction site. Modular construction that uses offsite manufacturing technologies should help to minimise the wastage, inefficiency and delays that affect on site construction. Production can happen in parallel with site preparation – speeding up construction and reducing disruption. Some reports have suggested that by building prefabricated modules off-site, construction times can be reduced by as much as 50% and costs cut by up to 20%.

The adoption of offsite manufacturing and prefabrication may ultimately be a partial solution for the construction industry’s skills and productivity gap, and for achieving sustainability goals. The shortage of skilled labour has restricted productivity in the sector, which has been largely flat for the last 20 years. The comparable improvement in industrial manufacturing has been more than 25% and automotive has been over 45%. On the downside, prefabrication will undoubtedly introduce greater product complexity for the manufacturers, but this would not be out of line with the operations for other highly engineered products with extensive bills of material (BOMs).

Perhaps the most important facet, and the one that will also underpin the developments described above, is the adoption and embedding of digital technologies and tools throughout the value chain:

- Building information modelling (BIM) and other digital techniques that enable design, construction, and supply chain teams to work more efficiently, while creating ‘digital twins’ for the subsequent benefit of operations, maintenance, and end-of-life activities.

- The deployment of robotics on construction sites with the use of autonomous vehicles and machinery, assembling robots, drones, and exoskeletons for worker augmentation.

- With tighter environmental regulations and the pressure to integrate ‘circular economy’ thinking, such tools should drive improvements in safety, quality, and productivity during construction, and support a ‘whole life’ approach to asset performance.

- Digital customer platforms that will enable suppliers to increase direct sales, reducing the importance of merchants, while benefitting from more integrated and collaborative planning and forecasting processes.

- Automation and analytics tools to help optimise throughput, thermal process energy costs, and quality in the manufacture of building products.

A more fundamental lesson, drawn from our more than fifty years of management consulting, is that any organisation, system, procedure or individual left undisturbed for just a few years will become inefficient. Construction and building materials is of course a mature sector, and although there has been marked consolidation and other changes of ownership in the market in Europe over the past decades, operational activities and working practices have largely remained unchanged.

Many of our assignments have therefore focused on examining overheads, organisational structures and processes, and the options for reducing costs and improving operational performance – while enhancing outputs and the service to customers. Benchmarks, whether external to the organisation or internal comparators, are often useful in this endeavour, and we can draw on a broad body of relevant knowledge and data for this purpose.

Where the work is required to be more transformative in nature, we provide input and guidance on fundamental organisational design and the development of a ‘Target Operating Model’. We have undertaken market surveys and research on customer expectations and requirements for several leading construction companies, not only to test and validate strategic initiatives, but also to inform structural design, and the underlying performance measures, incentives and managerial controls that go with this. Operating models and the governance structures and reporting arrangements that go with them are of course having to adapt, as corporate and business strategies more rigorously embrace sustainability and broader social value.

Another recurring theme in our work in the sector, both in the UK and internationally, has been the discipline of integrating acquisitions. This capability has more recently helped us develop strong relationships with a broad range of players, including inward investors and private equity firms. Expanding from this post-deal activity to pre-deal work, we have also completed a number of operational due diligence exercises, both on the buy-side and on the sell-side. The vendor due diligence process has grown in popularity in recent years as it gives sellers control of the narrative and the flow of information to potential buyers and helps position the upside opportunities for further evolution of a business.

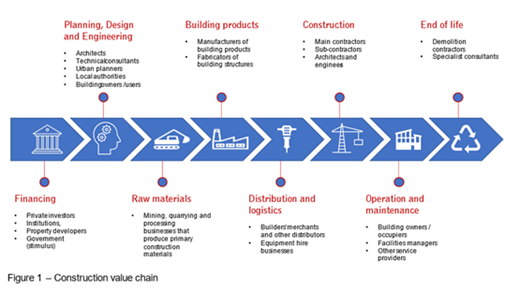

In the future we will remain a relevant and trusted partner to clients in the sector, working throughout all elements of the value chain (figure 1 below) and ensure that the experience and insight that we can bring to bear supports this positioning. It is likely that many of the challenges the sector faces will simply change the context and shift priorities for the work we do, while the business fundamentals and the functional skills and capabilities required stay the same. Elsewhere, it will require new skills and new approaches, and an ongoing recalibration of what constitutes ‘best practice’.